A couple of weeks ago, I gave a keynote at Droidcon, the (so far) largest Android conference, in Berlin. I spoke about why brands should look at it (I posted it here). Brands care for volume. They’re not necessarily interested in small segments of the market.

A couple of weeks ago, I gave a keynote at Droidcon, the (so far) largest Android conference, in Berlin. I spoke about why brands should look at it (I posted it here). Brands care for volume. They’re not necessarily interested in small segments of the market.

The iPhone is not an exception, it is rather a powerful reinforcement of that idea: in spite of its niche, it provides ROI (and warm, fluffy PR as well as content execs) when you compare the cost of the activity (creating an app) with its effects. The conclusion is however not that the iPhone is such a big driver in itself but that EVEN the iPhone (with its very limited scale) generates positive ROI.

The mobile phone market (and its associated content offerings) is extremely fragmented. A plethora of platforms (J2ME, BREW, Symbian, Blackberry, Windows Mobile, iPhone, Android, a couple of proprietary ones, some with middleware, now Bada and Maemo; wonderful…) and distribution channels (traditionally carriers, and lots of them, plus D2C distributors like Thumbplay, Jamba, Zed, Buongiorno, etc and now, increasingly, app stores: everything from the App Store to Android Market, Ovi, Blackberry App World and countless others). Tough for brands: they do not really care for a subset of users consisting of owners of J2ME devices on, say, Orange UK (no offence, Orange).

The ecosystem is tough to address as every mobile game developer will tell you. Which is why the iPhone was such a huge game changer: one device on one platform with one distribution channel globally. And all presented well, easy to use, great UI and users get to content with very few clicks and without unnecessary warnings). It is also always connected (rather than only connected in theory) and hence opens the doors to a new way of consuming, promoting and using content, specifically interactive one such as games and apps. Everyone else scrambles to follow but they struggle because it is such a different way to look at the world (well, different when you are a network operator or handset OEM). And because of this, competition on this platform is now fierce, very fierce.

The ecosystem is tough to address as every mobile game developer will tell you. Which is why the iPhone was such a huge game changer: one device on one platform with one distribution channel globally. And all presented well, easy to use, great UI and users get to content with very few clicks and without unnecessary warnings). It is also always connected (rather than only connected in theory) and hence opens the doors to a new way of consuming, promoting and using content, specifically interactive one such as games and apps. Everyone else scrambles to follow but they struggle because it is such a different way to look at the world (well, different when you are a network operator or handset OEM). And because of this, competition on this platform is now fierce, very fierce.

But now then, why would one support Android? I mean, Gameloft just said it sucks (well, commercially at least). Why do I think it will be (is?) big? And why do I think one should look at it now rather than, well, later?

For starters: it took Gameloft a full 3 days or so to realize the mess it made with its announcement to cut back Android; and swiftly issuing a statement that said pretty much the contrary… But, heck, we’re not running everywhere where Gameloft runs, do we?

Android’s potential is enormous! Not because Eric Schmitt, Google’s CEO said so. But because it is O.P.E.N. This gives it a potential that is beyond all others: it enjoys wide support from vendors (HTC, Dell, LG, Samsung, Sony Ericsson, Huawei, Motorola, Acer, Creative and countless more), carriers (it’s a little like the who’s who: China Mobile, China Unicom, NTT DoCoMo, Sprint, KDDI, Softbank, T-Mobile, TIM, Telefonica, Vodafone) and has a very powerful sponsor indeed in Google. The result is a huge number of devices (cf. Wikipedia page here), and they will grow. They will grow faster than Apple can because of the law of big numbers. Even if Apple may retain an edge on running the overall sexiest package but it will not withstand the overall numbers. Incidentally, the afore distinguishes Android – for the time being – from Symbian (which is now also open source): it lacks a convinced sponsor at the moment (Nokia seems to be wavering in its support) and also seems a little clunky (no open can be so strong so as to support a weak or rather outdated proposition). However, with its massive install base of 280m+ devices it could rebound if they fix this.

Android stretches further though: it is not limited to mobile devices, it goes across to eBook readers, set-top boxes, netbooks, you name it. Users increasingly swap between screens. As a content and/or service provider, you want to be with them, be of service to them, wherever they are. They should not have to worry, you should! Android makes this relatively easy for you.

The Power of Open is tremendous. It provides for (theoretically) infinite growth. And you want to be there. And you want to be there now: They say, a tidal wave of apps is coming. You won’t catch the train once you can see it… 😉

Do not forget: people (and brands) want to reach people. Full stop. They do not necessarily want to reach people who happen to have an XYZ device running the ABC OS on the carrier X in country Y! Apple is wonderful (I am an avid iPhone user and do not plan to change – well, yet) but it is a niche. And if you have business to do, you may want to look beyond that niche.

Do not forget: people (and brands) want to reach people. Full stop. They do not necessarily want to reach people who happen to have an XYZ device running the ABC OS on the carrier X in country Y! Apple is wonderful (I am an avid iPhone user and do not plan to change – well, yet) but it is a niche. And if you have business to do, you may want to look beyond that niche.

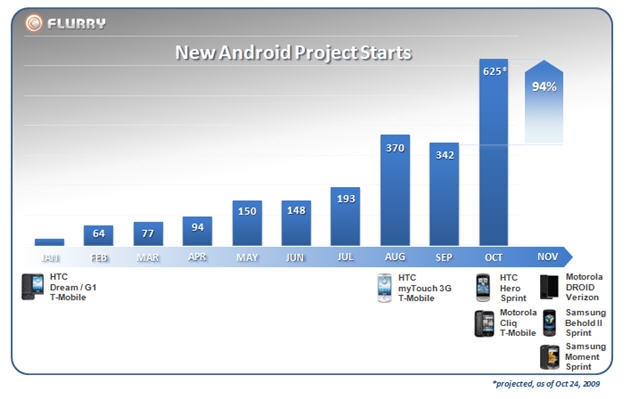

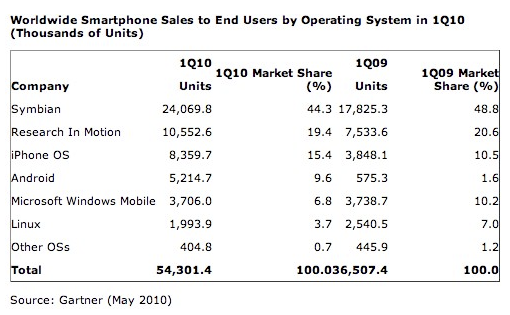

According to a recent

According to a recent  So what about it? Let us not forget how young Android is – even compared to the adolescent iPhone. The

So what about it? Let us not forget how young Android is – even compared to the adolescent iPhone. The  Also, do not forget the big brands: they do not necessarily care for a small share of the audience only. Whilst Android was fledgling and just starting up, they may have held back but, ultimately, they are about reach, and Android is certainly bound to deliver that. I would therefore suggest that we will be seeing an influx of large brands (gaming and otherwise) onto the Android platform very soon, and this will also help user orientation as to what to go for and what not.

Also, do not forget the big brands: they do not necessarily care for a small share of the audience only. Whilst Android was fledgling and just starting up, they may have held back but, ultimately, they are about reach, and Android is certainly bound to deliver that. I would therefore suggest that we will be seeing an influx of large brands (gaming and otherwise) onto the Android platform very soon, and this will also help user orientation as to what to go for and what not. The billing side of things is bound to improve, too. With carrier-billing around the corner (cf. supra), this will get easier and better. And also easier and better than it is on the iPhone: charges will simply appear on your carrier bill (smart pipe anyone?). Besides that, the business models for games are undergoing significant changes anyhow: Freemium takes centre-stage, and so it should: the model allows people to try a game out and be charged for it only when they know that a) they like it, b) what they are being charged for (e.g. that coveted sword, a couple of precious lives, or that cool background theme).

The billing side of things is bound to improve, too. With carrier-billing around the corner (cf. supra), this will get easier and better. And also easier and better than it is on the iPhone: charges will simply appear on your carrier bill (smart pipe anyone?). Besides that, the business models for games are undergoing significant changes anyhow: Freemium takes centre-stage, and so it should: the model allows people to try a game out and be charged for it only when they know that a) they like it, b) what they are being charged for (e.g. that coveted sword, a couple of precious lives, or that cool background theme).