I have been dealing with movie and TV licenses for longer than I care to remember, and the pattern (with few exceptions) always was the same: the licensor comes to you saying that, because they are offering you (the publisher) a well-known movie/TV/entertainment property that everyone and their dog are fans of, you should pay them a healthy amount of money (either up-front or as a minimum guarantee against revenues) for them to grant you that license. This means that the publisher starts at a point of significant loss: a six-figure guarantee (and I’ve seen larger ones, too), six-figure production costs and little mitigating the risk that the title might totally tank.

I have been dealing with movie and TV licenses for longer than I care to remember, and the pattern (with few exceptions) always was the same: the licensor comes to you saying that, because they are offering you (the publisher) a well-known movie/TV/entertainment property that everyone and their dog are fans of, you should pay them a healthy amount of money (either up-front or as a minimum guarantee against revenues) for them to grant you that license. This means that the publisher starts at a point of significant loss: a six-figure guarantee (and I’ve seen larger ones, too), six-figure production costs and little mitigating the risk that the title might totally tank.

However, in the “old” world (scil. pre-app stores “as made famous by the iPhone”), people considered themselves to be lucky to get their hands on a well-known property as it would at least guarantee one thing, and that was “deck placement”, namely a good coverage across those coveted feature slots on carrier decks around the world. If you had the distribution network and delivered the package, you had a decent chance of making your money back (this even worked with a rotten game that was based on a movie license for a hilariously successful movie).

All new in the App Store World

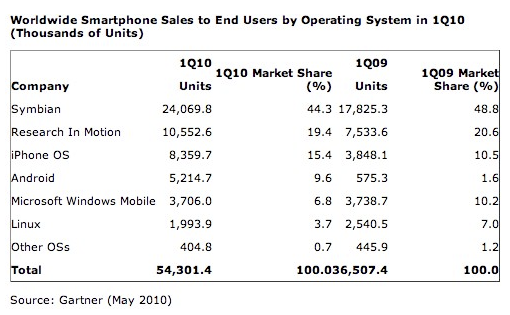

Enter the “new” world of OS-driven app stores. The formidable Jeremy Laws published estimates of how movie & TV-license-based games were faring on the Apple App Store, and the results are – though not horrendous – humbling indeed. Only a good half dozen titles broke into the top 20 (by sales) in all of 2010. Not a single one ranked in the top 150 (!) of the top-grossing category. The average revenue was estimated by him to hit $1.3m. Now, don’t let yourself be blinded by this 7-figure amount: top-tier movie titles don’t often come cheap and the games behind them need to be reasonably faithful to the blueprint the movie gives you. Otherwise, the IP owner will not approve the game and the revenues will be, well, non-existent. Add to that a revenue share that the IP owner will earn even if the aforementioned guarantees are being settled, it slims down the margins fairly dangerously.

IP Doesn’t Pull as It Used to, or Does It?

The big news is however that the old formula big license + some sort of game = exposure does obviously no longer work (at least not in the same semi-automated way as was the case). With decent relationships into Apple, a good game for a good movie might still get a feature slot somewhere. However, the fact that none of the titles sampled in the above blog post were anywhere close to the top-grossing list shows that the pulling power has greatly diminished. How’s that?

Movie studios and TV production houses (and not only them: sports clubs are good at that, too) traditionally view a license as secondary exploitation of their intellectual property. The rule of thumb for a movie was that the box office should recoup the production costs and the secondary exploitation (DVD, TV rights, merchandise and, well, licenses) would provide for the profits. It is very much an analogue approach in which a scarce good is and will remain scarce unless its producer will (can?) change that scarcity. It does not translate well to the fluidity of a digital environment (with, normally, many more alternatives to access and consume media). It worked in old-world mobile because that ecosystem functioned very similar to a vertical supply chain. No more.

Game publishers suffer (or at least some of them) suffer from a similar perception issue: we have always done it that way… Well then…

A License is a Brand Extension

However, the huge differentiator is the ability to use (and exploit) the interactivity digital media offer and use it as a marketing and promotional channel. Now, a simple adaptation of the movie’s theme into a (traditional) game will not cut this. But more innovative approaches that utilise the ability to communicate with fans opens so many more doors to a) maximise the core proposition (selling cinema tickets, DVDs, digital downloads and such like) and bind people to the brand for longer (which is a potentially huge win for the cyclical movie business).

So, Jeremy’s charts “only” show us that only a few (if any) of the IP owners (and, arguably, publishers) “got” that so far. The opportunities for such an approach are huge.

What anyone who speaks to rights owners over licensing movie and TV properties should do though is take a copy of that chart for your negotiations. And then tell them how they should really treat it: it is a brand extension that leverages the core IP rather than a meagre spin-off license! Seen this way, there is significant opportunity for studios to secure their primary revenue streams and build a new rapport to their audiences. In particular the latter surely is of a value that exceeds six-figure guarantees anyhow.

So I guess we have to thank the iPhone again for breaking open yet another paradigm. And it was time for that, too!

Step 2: tariffs. With an unhealthy amount of traveling abroad to do, my main cost item on phone bills regularly is data roaming, so this is where my sensitivity lies (because of the eye-watering bills I regularly get, I am not bothered about 600 or 900 UK any-network minutes costing £5 more or less), and it became clear quickly: Orange, T-Mobile and 3 are out of the race (their charges are even higher than O2’s). Vodafone looks good (about 1/3 of O2’s rates) but O2 claims to still have their Blackberry tariff for international data roaming (although I struggled to find it on their website). Now, THAT would bring my bill down by a cool £150-200 a month or so. Enter Blackberry. The

Step 2: tariffs. With an unhealthy amount of traveling abroad to do, my main cost item on phone bills regularly is data roaming, so this is where my sensitivity lies (because of the eye-watering bills I regularly get, I am not bothered about 600 or 900 UK any-network minutes costing £5 more or less), and it became clear quickly: Orange, T-Mobile and 3 are out of the race (their charges are even higher than O2’s). Vodafone looks good (about 1/3 of O2’s rates) but O2 claims to still have their Blackberry tariff for international data roaming (although I struggled to find it on their website). Now, THAT would bring my bill down by a cool £150-200 a month or so. Enter Blackberry. The  And then I started to compromise: anything exclusive to Orange, T-Mobile or 3 was out of the question (because data roaming is pretty much a killer for me), which boils it down to Blackberry and O2 or any of the others on Vodafone (which would mean that I couldn’t get what started being my favourite, the Samsung Omnia 7). Hang on: I compromise over some shoddy pounds? Is the handset then not so all important as one might have believed when reading all those blogs, news blitzes and tech publications over the last months?

And then I started to compromise: anything exclusive to Orange, T-Mobile or 3 was out of the question (because data roaming is pretty much a killer for me), which boils it down to Blackberry and O2 or any of the others on Vodafone (which would mean that I couldn’t get what started being my favourite, the Samsung Omnia 7). Hang on: I compromise over some shoddy pounds? Is the handset then not so all important as one might have believed when reading all those blogs, news blitzes and tech publications over the last months? Sluggishly reacting applications, latency in almost everything you do, crashes, blank screens, long lag to pick up networks, buggy settings. Do you remember any of this? Sounds like some old-fashioned feature phone that was somewhat overloaded by its ambitious maker, doesn’t it? But, alas, no, it is not. This is the user experience with a one-year-old iPhone 3G, 16GB since 24 June 2010. Do you recognise the date? Then luck will have it that you have experienced the same: the grandly titled “iOS4” update that was being pushed down your throat (or rather iTunes) to your iPhone 3G.

Sluggishly reacting applications, latency in almost everything you do, crashes, blank screens, long lag to pick up networks, buggy settings. Do you remember any of this? Sounds like some old-fashioned feature phone that was somewhat overloaded by its ambitious maker, doesn’t it? But, alas, no, it is not. This is the user experience with a one-year-old iPhone 3G, 16GB since 24 June 2010. Do you recognise the date? Then luck will have it that you have experienced the same: the grandly titled “iOS4” update that was being pushed down your throat (or rather iTunes) to your iPhone 3G. And then it came back to bite them! I am not a techie but iOS4 on the iPhone 3G feels like someone put a little too much luggage onto too frail a porter: the things creaks and aches at every corner. Gone are the days where one could switch from one app to another in seconds, where the iPhone – in good Apple style – did what you wanted it to do without much ado but breathtaking efficiency and speed. Now, it is clunky and, well, very old-fashioned. It could of course all have been avoided: just don’t push iOS4 to the iPhone 3G (or older models). No one would have cried, you should think: if the hardware cannot handle it, it cannot handle it. Users understand such things one should think. Keep iOS4 to the iPhone 4 (even the numbers match, doh!).

And then it came back to bite them! I am not a techie but iOS4 on the iPhone 3G feels like someone put a little too much luggage onto too frail a porter: the things creaks and aches at every corner. Gone are the days where one could switch from one app to another in seconds, where the iPhone – in good Apple style – did what you wanted it to do without much ado but breathtaking efficiency and speed. Now, it is clunky and, well, very old-fashioned. It could of course all have been avoided: just don’t push iOS4 to the iPhone 3G (or older models). No one would have cried, you should think: if the hardware cannot handle it, it cannot handle it. Users understand such things one should think. Keep iOS4 to the iPhone 4 (even the numbers match, doh!). However, I think that is not it. My suspicion is rather more frightening. It very much feels like Apple starting to overextend itself and learn how complex and fragile it is to deal in the mobile space. Pushing iOS4 to devices that obviously (not only under some special and hard to find circumstances) cannot cope with it is just shoddy. Every game or app developer in the market for more than 2 years would have caught this in QA. Does Apple not have QA? Or not anymore? Or at least not enough? It might happen to you when you try too much too quickly. Apple’s passion (or paranoia?) that drives it to try and do everything itself appears to haunt it now: I mean, QA is really simple. You don’t need cohorts of phDs in elementary physics to do this. It doesn’t take you 3 years to build it up. And – last but not least – Apple appeared to being very much on top of this in the past. So what happened?

However, I think that is not it. My suspicion is rather more frightening. It very much feels like Apple starting to overextend itself and learn how complex and fragile it is to deal in the mobile space. Pushing iOS4 to devices that obviously (not only under some special and hard to find circumstances) cannot cope with it is just shoddy. Every game or app developer in the market for more than 2 years would have caught this in QA. Does Apple not have QA? Or not anymore? Or at least not enough? It might happen to you when you try too much too quickly. Apple’s passion (or paranoia?) that drives it to try and do everything itself appears to haunt it now: I mean, QA is really simple. You don’t need cohorts of phDs in elementary physics to do this. It doesn’t take you 3 years to build it up. And – last but not least – Apple appeared to being very much on top of this in the past. So what happened? Anyway, back to Vodafone. They have realised (and, credit to them, admit it!) that a vertical implementation where you only get the full scope of 360 services if you have one of two phones doesn’t work. And, well, that’s somewhat obvious, isn’t it? Or is it a reasonable assumption that all my friends will all of a sudden (and at the same time) exchange their various handsets for a Samsung M1? No, I thought not either.

Anyway, back to Vodafone. They have realised (and, credit to them, admit it!) that a vertical implementation where you only get the full scope of 360 services if you have one of two phones doesn’t work. And, well, that’s somewhat obvious, isn’t it? Or is it a reasonable assumption that all my friends will all of a sudden (and at the same time) exchange their various handsets for a Samsung M1? No, I thought not either. On a sideline: I will be moderating a panel on “How to Make Money as a Developer” this week at

On a sideline: I will be moderating a panel on “How to Make Money as a Developer” this week at  Apple’s iPhone is only a marketing fad for vain urbanites. True purists go for Android. Those who see the light in volume go for Nokia or Samsung.

Apple’s iPhone is only a marketing fad for vain urbanites. True purists go for Android. Those who see the light in volume go for Nokia or Samsung. On the Nexus, you’re OK (-ish) if your life evolves around Google. With a Gmail account and associated contacts (and/or calendars), you’re sort of OK. It does all that. Now – shock, horror – I do not actually send all my mail from Gmail and my contacts are mainly dealt with in my address book (take Outlook or whatever you want if you’re a Windows user). And I use iCal and not Google Calendar. And so it starts: there is no desktop application that would help me do this. On a Mac, the phone is not even recognised when you plug it in (and that is a rare thing on a Mac; is this another piece of Apple vs. Google? I don’t know but I doubt it). So you are finding yourself setting everything up by hand! Entering the POP3 and SMTP (or IMAP) server addresses, user names, passwords, etc, etc for seven e-mail accounts is no fun. And (remember I am not a techie) invariably leads to some box checked wrongly here or a typo in a password there and, kawoom, nothing works. I can set up a Google Calendar/iCal sync BUT that will only sync the specific Google Calendar bit between the two, and not any of my other (work, home) calendars. I can sync my address book with Google, so that works. The whole procedure took me the better part of 45 minutes, including lots of corrections and swearing and led to me abandoning a half-configured beauty of an Android phone. Great result.

On the Nexus, you’re OK (-ish) if your life evolves around Google. With a Gmail account and associated contacts (and/or calendars), you’re sort of OK. It does all that. Now – shock, horror – I do not actually send all my mail from Gmail and my contacts are mainly dealt with in my address book (take Outlook or whatever you want if you’re a Windows user). And I use iCal and not Google Calendar. And so it starts: there is no desktop application that would help me do this. On a Mac, the phone is not even recognised when you plug it in (and that is a rare thing on a Mac; is this another piece of Apple vs. Google? I don’t know but I doubt it). So you are finding yourself setting everything up by hand! Entering the POP3 and SMTP (or IMAP) server addresses, user names, passwords, etc, etc for seven e-mail accounts is no fun. And (remember I am not a techie) invariably leads to some box checked wrongly here or a typo in a password there and, kawoom, nothing works. I can set up a Google Calendar/iCal sync BUT that will only sync the specific Google Calendar bit between the two, and not any of my other (work, home) calendars. I can sync my address book with Google, so that works. The whole procedure took me the better part of 45 minutes, including lots of corrections and swearing and led to me abandoning a half-configured beauty of an Android phone. Great result. My answer is: because they design it with engineer-centric design. And that is wrong! Why? Well, because most people are not engineers! An engineer thinks something along the following: I am Google and we love the cloud. Therefore, I will design everything so that it will adhere to that principle and will – in a purist kind of way – design everything in a way that you can beautifully and seamlessly set everything up – if and as long as you use all the wonderful Google services we have. And if you don’t get that, you’re not worthy.

My answer is: because they design it with engineer-centric design. And that is wrong! Why? Well, because most people are not engineers! An engineer thinks something along the following: I am Google and we love the cloud. Therefore, I will design everything so that it will adhere to that principle and will – in a purist kind of way – design everything in a way that you can beautifully and seamlessly set everything up – if and as long as you use all the wonderful Google services we have. And if you don’t get that, you’re not worthy. Apple looks at things a little differently (and it is not only for the better although, for most people, it is): they provide a tool that brings everything I need over to my phone just like that. Job done. Easy! They will look at whatever tools they need for this. And if it means extending iTunes (which, yes, I know, they had already) to accommodate syncing data other than music and video to something other than a computer, than so be it. In that, they follow their own philosophy as slavishly as the other guys do but they do design it from a people-centric rather than an engineer-centric point of view. And that is why it works so well for people that are not (also) engineers.

Apple looks at things a little differently (and it is not only for the better although, for most people, it is): they provide a tool that brings everything I need over to my phone just like that. Job done. Easy! They will look at whatever tools they need for this. And if it means extending iTunes (which, yes, I know, they had already) to accommodate syncing data other than music and video to something other than a computer, than so be it. In that, they follow their own philosophy as slavishly as the other guys do but they do design it from a people-centric rather than an engineer-centric point of view. And that is why it works so well for people that are not (also) engineers.

According to a recent

According to a recent  So what about it? Let us not forget how young Android is – even compared to the adolescent iPhone. The

So what about it? Let us not forget how young Android is – even compared to the adolescent iPhone. The  Also, do not forget the big brands: they do not necessarily care for a small share of the audience only. Whilst Android was fledgling and just starting up, they may have held back but, ultimately, they are about reach, and Android is certainly bound to deliver that. I would therefore suggest that we will be seeing an influx of large brands (gaming and otherwise) onto the Android platform very soon, and this will also help user orientation as to what to go for and what not.

Also, do not forget the big brands: they do not necessarily care for a small share of the audience only. Whilst Android was fledgling and just starting up, they may have held back but, ultimately, they are about reach, and Android is certainly bound to deliver that. I would therefore suggest that we will be seeing an influx of large brands (gaming and otherwise) onto the Android platform very soon, and this will also help user orientation as to what to go for and what not. The billing side of things is bound to improve, too. With carrier-billing around the corner (cf. supra), this will get easier and better. And also easier and better than it is on the iPhone: charges will simply appear on your carrier bill (smart pipe anyone?). Besides that, the business models for games are undergoing significant changes anyhow: Freemium takes centre-stage, and so it should: the model allows people to try a game out and be charged for it only when they know that a) they like it, b) what they are being charged for (e.g. that coveted sword, a couple of precious lives, or that cool background theme).

The billing side of things is bound to improve, too. With carrier-billing around the corner (cf. supra), this will get easier and better. And also easier and better than it is on the iPhone: charges will simply appear on your carrier bill (smart pipe anyone?). Besides that, the business models for games are undergoing significant changes anyhow: Freemium takes centre-stage, and so it should: the model allows people to try a game out and be charged for it only when they know that a) they like it, b) what they are being charged for (e.g. that coveted sword, a couple of precious lives, or that cool background theme).