Earlier this week, I gave a talk at the Mobile Gaming Conference at ICE, the premier i-gaming (that’s gambling to you and I) event in London. Below, you will find the slides to the talk.

Let me outline briefly though why I think that social elements to gaming is something that I find the gaming (as in gambling, real-money gaming, etc) sector should be excited about (and it was hard to tell if many people were; ’nuff said):

“Social” games work if they address or are based upon a community of sorts. This needs to be supported by the game design and its mechanic as well as through tools that actually allow those communal juices to flow (and, yes, that’s what we at Scoreloop are doing and that’s why I am preaching about the subject so regularly). Now, the gaming folks have a lot of this sitting on a big silver plate right under their noses: “proper” gamers, i.e. those who spend money on their pastime, are tied together by that particular passion (this of course equally applies to all those passionate about lost puppies, cows and golden eggs…). For the real-money folks, there is also the billing side to consider: their clientele is used and quite willing to pay, and a billing relationship is often already in place.

The addition of social elements to such “real” games can essentially do two things then:

Cement existing customer base and avoid promiscuity of users

I have been hearing this a lot: users on, say, real-money poker sites often play on multiple sites. This is painful to the gaming operators as they spend considerable amounts recruiting their folks. It is a race to the bottom (of sustainable margins) and the adjustment mechanisms are scarce and largely reduced to bounties and clever marketing. Adding social elements adds that glue that increases the likelihood that players will stay with you. Why? Because they receive value over and above the core proposition: they feel better nestled into their community, which is – albeit a little intangible – real and not only perceived value. Incidentally though, it is also value that is not that expensive to create (cf. above under “margins, low).

Attract new users

Outside the hard core of gamers, there is a whole lot of people who are quite content to play for fun (Zynga Poker still has more active users than most “real” poker sites combined). Funnily enough, Zynga also makes more money with its soft version than a lot of gaming operators do with its real one. This is because a) they tie it into the social graph and b) a lot of users just like to play for fun – but they still spend money, only in more manageable increments.

I suggest that this is a major entry gate for gaming operators to attract new users (though I do not suggest that “hooking” people is something good!). A softer approach that introduces many shades of grey rather than only offering black and white will make it so much more compelling to play, properly or only trying it out and the very folks that are in the prime spot to capture these users (because they have all the experience, background and know-how) leave a lot of money on the table there (pun indeed intended).

But now, without any further ado, here are the slides:

For those of you who like that better, I have also uploaded it to Sribd here.

A couple of weeks ago, I gave a keynote at

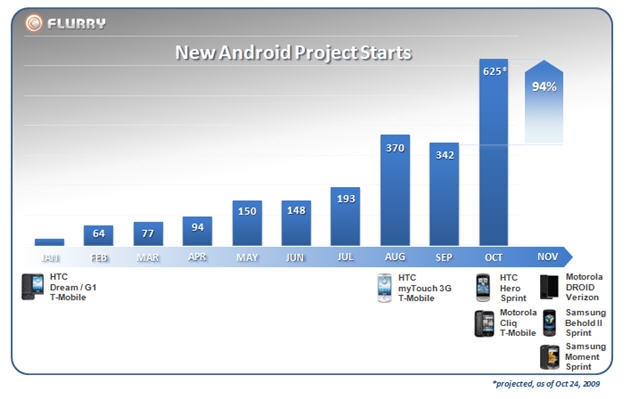

A couple of weeks ago, I gave a keynote at  The ecosystem is tough to address as every mobile game developer will tell you. Which is why the iPhone was such a huge game changer: one device on one platform with one distribution channel globally. And all presented well, easy to use, great UI and users get to content with very few clicks and without unnecessary warnings). It is also always connected (rather than only connected in theory) and hence opens the doors to a new way of consuming, promoting and using content, specifically interactive one such as games and apps. Everyone else scrambles to follow but they struggle because it is such a different way to look at the world (well, different when you are a network operator or handset OEM). And because of this, competition on this platform is now fierce, very fierce.

The ecosystem is tough to address as every mobile game developer will tell you. Which is why the iPhone was such a huge game changer: one device on one platform with one distribution channel globally. And all presented well, easy to use, great UI and users get to content with very few clicks and without unnecessary warnings). It is also always connected (rather than only connected in theory) and hence opens the doors to a new way of consuming, promoting and using content, specifically interactive one such as games and apps. Everyone else scrambles to follow but they struggle because it is such a different way to look at the world (well, different when you are a network operator or handset OEM). And because of this, competition on this platform is now fierce, very fierce. Do not forget: people (and brands) want to reach people. Full stop. They do not necessarily want to reach people who happen to have an XYZ device running the ABC OS on the carrier X in country Y! Apple is wonderful (I am an avid iPhone user and do not plan to change – well, yet) but it is a niche. And if you have business to do, you may want to look beyond that niche.

Do not forget: people (and brands) want to reach people. Full stop. They do not necessarily want to reach people who happen to have an XYZ device running the ABC OS on the carrier X in country Y! Apple is wonderful (I am an avid iPhone user and do not plan to change – well, yet) but it is a niche. And if you have business to do, you may want to look beyond that niche. Why is this more significant? Because it is (like Google/AdMob) a cross-platform play that (unlike Google/AdMob) also expands the basis of business models deployed. Playfish derives the majority of its revenues from so-called virtual currencies, and in particular also from lead-generation deals (which recently have

Why is this more significant? Because it is (like Google/AdMob) a cross-platform play that (unlike Google/AdMob) also expands the basis of business models deployed. Playfish derives the majority of its revenues from so-called virtual currencies, and in particular also from lead-generation deals (which recently have