Recently, previously civilized and subtle top executives of the world’s big mobile handset makers took the gloves off and became, well, a little more outspoken. What sticks from this is, of course, always only the most figurative snippets. Because all of these esteemed people have the most vested of all vested interests, their statements tend to distort reality a little. And because of that, we have increasingly lively debates at hand. But, alas, these debates may not necessarily lead to enlightenment.

Recently, previously civilized and subtle top executives of the world’s big mobile handset makers took the gloves off and became, well, a little more outspoken. What sticks from this is, of course, always only the most figurative snippets. Because all of these esteemed people have the most vested of all vested interests, their statements tend to distort reality a little. And because of that, we have increasingly lively debates at hand. But, alas, these debates may not necessarily lead to enlightenment.

So I thought I undertake a little mapping exercise and see where we end up…

The War of Words

I don’t know who started this. But we have had a couple of outbursts recently. Nokia’s soon to be former smartphone maestro Anssi Vanjoki (of nGage and other fame) likened switching to Android to boys who pee in their pants for warmth in winter. What he wanted to say is that it gets worse after brief relief. Apple supremo Steve Jobs sees no one (and in particular not RIM) getting anywhere near his beautiful iPhones anytime soon (he probably has not forgotten Mike Lazaridis riposte to the iPhone 4’s Antennagate). Others are convinced that Apple cannot beat Android. Period. Everyone wonders what Nokia will come up with (and, no, we do not think the N8 is it). Etc, etc, etc.

A Lot of Little Worlds

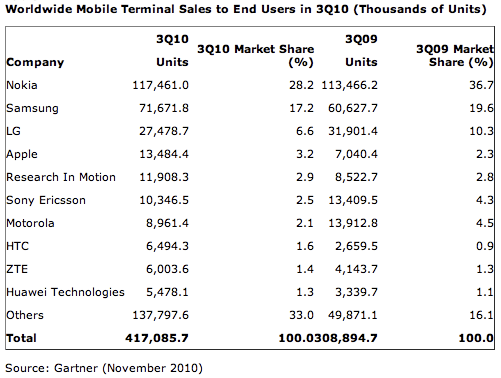

When one looks at the world map and then listens to the good folks cited above (and others), it appears that there is not one but many little worlds out there. Nokia is sitting high and dry in overall handset rankings with over 35% market share across all handsets. It is estimated to ship more than 500m handsets in 2011, too (so hold back with your obituary just yet). However, it is nowhere to be seen in the US (and even less in US smartphones where it is fighting a close fight with Palm around the 4-5% mark). Samsung (one of the few big boys not to participate in the above bickering) is building out its #2 spot with around 20% market share. Apple is well behind (although recording fairly impressive numbers given that it is basically a single handset company).

When one looks at the world map and then listens to the good folks cited above (and others), it appears that there is not one but many little worlds out there. Nokia is sitting high and dry in overall handset rankings with over 35% market share across all handsets. It is estimated to ship more than 500m handsets in 2011, too (so hold back with your obituary just yet). However, it is nowhere to be seen in the US (and even less in US smartphones where it is fighting a close fight with Palm around the 4-5% mark). Samsung (one of the few big boys not to participate in the above bickering) is building out its #2 spot with around 20% market share. Apple is well behind (although recording fairly impressive numbers given that it is basically a single handset company).

Does this matter in the discussion who is “winning”? No, it does not. An iPhone is useless if you are in an emerging (or developing) country with no 3G coverage and no abundance of power outlets from where to re-charge your fancy beauty every 8-12 hours or so. On the other end of the spectrum, a Nokia 1100 is useless if you would like to navigate on your handset through the urban jungle of Manhattan whilst shooting photos for the ones at home. But it runs forever, doesn’t mind a bit of sand or water and will never ever break. Ever.

The point is that there is more than one market here. The market is not mobile phones. The market is not even smartphones. There are many. And in some of them, Apple is looking really weak. And in others, Nokia is looking really weak.

Single Segment vs. Multi-Segment

Nokia’s strength (and, to an extent, curse) is that it wants to be everything to everyone. The N8 is a great handset from a hardware perspective but, after having played around with it for a week or so, I think it has a distinct 3-years-ago feel to it. It makes great phone calls though (which, well, the iPhone does not always). However, will Apple be able to challenge Nokia (and Samsung) in the broad lower-end mass market? Not for a long time, I would say.

The situation is a little more serious for other single-segment OEM. RIM used to live off the fat of the land in the enterprise sector. And it continues to thrive there. In recent years, it has seen a huge upswing amongst kids – because of the now almost legendary BBM (Blackberry Messenger for the uninformed). However, can you successfully build or expand on a single feature? And then on one that could really also be mimicked, worked around or substituted by something similar? Tricky.

The situation is a little more serious for other single-segment OEM. RIM used to live off the fat of the land in the enterprise sector. And it continues to thrive there. In recent years, it has seen a huge upswing amongst kids – because of the now almost legendary BBM (Blackberry Messenger for the uninformed). However, can you successfully build or expand on a single feature? And then on one that could really also be mimicked, worked around or substituted by something similar? Tricky.

Tricky in a different way is the situation for the likes of Motorola, HTC or Sony Ericsson: they have all committed their life to the Android platform. With Google’s muscle in the Open Handset Alliance, this means that they depend more and more on hardware design only. It feels a little like the movie business: hit-driven. And that is a tricky situation to be in. HTC looks good at this: this is home turf for it. On top of this, it has quickly started to try some gentle steps to distinguish itself (HTC Sense; Google Nexus One, etc) from other Android makers. Motorola’s Blur was less successful initially. And Sony Ericsson has yet to show its hand.

Tricky in a different way is the situation for the likes of Motorola, HTC or Sony Ericsson: they have all committed their life to the Android platform. With Google’s muscle in the Open Handset Alliance, this means that they depend more and more on hardware design only. It feels a little like the movie business: hit-driven. And that is a tricky situation to be in. HTC looks good at this: this is home turf for it. On top of this, it has quickly started to try some gentle steps to distinguish itself (HTC Sense; Google Nexus One, etc) from other Android makers. Motorola’s Blur was less successful initially. And Sony Ericsson has yet to show its hand.

Vertically Integrated vs. Multi-OEM

All this does of course not bother Android (and perhaps also Microsoft’s Windows Phone 7) as they have the advantage of being able to bringing many weapons to the battlefield. Android’s huge advantage is one of price due to its open-source nature: For Windows Phone 7, you need to pay a software license. Android is – basically – free. Both have multiple OEM that fight their corner though. Which is, or at least can be, good. Google will not really care if the next killer phone is produced by HTC or Motorola or Sony Ericsson (or Foxconn directly for that matter).

All this does of course not bother Android (and perhaps also Microsoft’s Windows Phone 7) as they have the advantage of being able to bringing many weapons to the battlefield. Android’s huge advantage is one of price due to its open-source nature: For Windows Phone 7, you need to pay a software license. Android is – basically – free. Both have multiple OEM that fight their corner though. Which is, or at least can be, good. Google will not really care if the next killer phone is produced by HTC or Motorola or Sony Ericsson (or Foxconn directly for that matter).

Apple will likely struggle to match the sheer number of iterations being thrown at it. And therefore it is likely that Android will be winning, or rather continue to win.

Does this matter much to Apple? Possibly not. The margin discussion will, in all likelihood, be one that Apple execs will happily take. They will look better at it. However, will it manage to break the old Mac vs. PC pattern? Probably not. However, Apple’s position looks much brighter than it did in the decades of 5% OS-share mediocrity. The company has perfected the hardware-software-service-sex-appeal equation, which looks likely to cement a much more comfortable niche for it (just have a look at its market cap).

Does this matter much to Apple? Possibly not. The margin discussion will, in all likelihood, be one that Apple execs will happily take. They will look better at it. However, will it manage to break the old Mac vs. PC pattern? Probably not. However, Apple’s position looks much brighter than it did in the decades of 5% OS-share mediocrity. The company has perfected the hardware-software-service-sex-appeal equation, which looks likely to cement a much more comfortable niche for it (just have a look at its market cap).

Vertically Integrated Multi-Segment

Nokia and Samsung try (or seem to try) a different way. Nokia is betting on MeeGo (its Symbian support sounds more and more hollow by the day). Samsung, which traditionally bet on almost every horse, made a big push for its proprietary bada OS.

This approach could be a winner: with their strong grip on emerging markets and the ability to roll out a proprietary OS across multiple segments, it presents an opportunity to nurture users in emerging markets (where the real growth will be in the next 5 years) into the use of their respective ecosystems. It did pay off for Nokia the first time around!

The Real Battlefield

In the more saturated markets in the Northern hemisphere though the battlefield is likely to be one involving OEM and network operators. This is where Apple really shook up the markets. A lot of the revenue streams from the iPhone simply bypass carriers. The Android OS opens similar avenues. The reason why Apple managed to pull this off is likely to be seen in the branding side of things: it enjoys such pulling power that carriers were bending over backwards to get their hands onto it (and then of course started moaning about the strain on their networks). Android is now being positioned as the alternative. At least, carriers can put competing offers onto Android devices.

Now, in markets where handset purchases are also driven by the overall package (cf. my recent post on this), this is likely to be important.

Nokia, Motorola, RIM, Samsung, etc all enjoy good distribution relationships with carriers. Apple is in a special position because of a) its brand but also b) its price; not much flexibility here, I suspect.

Nokia for instance struggled however to assert itself with some further-reaching ideas it had: some carriers pushed it back over e.g. plans to put Skype onto its handsets. It apparently has less brand power than Apple. Or the carriers were more used to having a say over what gets onto its handsets and what doesn’t.

Conclusion: We don’t Know What We don’t Know

We are, hence, in essence still in a fairly foggy situation: other than Apple’s brand power, we really don’t know as yet what, who, how will prevail. And that is in itself good news. Because it means we will have some time left with competing concepts, competing OEM and competing approaches. And with more CEO banter of course…

You hear it often (most recently by Average Jane): people who complain about unwanted features and complexities of mobile phones. And now here comes a company (not your ordinary OEM, mind you) who is bringing out just that: the ultimate dumbphone (I am referring to features not potential users). Meet John Doe’s new phone, the anti-smartphone: Dutch agency John Doe (sic!) premiered John’s Phone, which can do, well, make and receive phone calls. SMS? No. Address book? Yes, from paper with a pocket to stick it in at the back. Java? No. Apps? No. Anything other than making phone calls? No.

You hear it often (most recently by Average Jane): people who complain about unwanted features and complexities of mobile phones. And now here comes a company (not your ordinary OEM, mind you) who is bringing out just that: the ultimate dumbphone (I am referring to features not potential users). Meet John Doe’s new phone, the anti-smartphone: Dutch agency John Doe (sic!) premiered John’s Phone, which can do, well, make and receive phone calls. SMS? No. Address book? Yes, from paper with a pocket to stick it in at the back. Java? No. Apps? No. Anything other than making phone calls? No.

Step 2: tariffs. With an unhealthy amount of traveling abroad to do, my main cost item on phone bills regularly is data roaming, so this is where my sensitivity lies (because of the eye-watering bills I regularly get, I am not bothered about 600 or 900 UK any-network minutes costing £5 more or less), and it became clear quickly: Orange, T-Mobile and 3 are out of the race (their charges are even higher than O2’s). Vodafone looks good (about 1/3 of O2’s rates) but O2 claims to still have their Blackberry tariff for international data roaming (although I struggled to find it on their website). Now, THAT would bring my bill down by a cool £150-200 a month or so. Enter Blackberry. The

Step 2: tariffs. With an unhealthy amount of traveling abroad to do, my main cost item on phone bills regularly is data roaming, so this is where my sensitivity lies (because of the eye-watering bills I regularly get, I am not bothered about 600 or 900 UK any-network minutes costing £5 more or less), and it became clear quickly: Orange, T-Mobile and 3 are out of the race (their charges are even higher than O2’s). Vodafone looks good (about 1/3 of O2’s rates) but O2 claims to still have their Blackberry tariff for international data roaming (although I struggled to find it on their website). Now, THAT would bring my bill down by a cool £150-200 a month or so. Enter Blackberry. The  And then I started to compromise: anything exclusive to Orange, T-Mobile or 3 was out of the question (because data roaming is pretty much a killer for me), which boils it down to Blackberry and O2 or any of the others on Vodafone (which would mean that I couldn’t get what started being my favourite, the Samsung Omnia 7). Hang on: I compromise over some shoddy pounds? Is the handset then not so all important as one might have believed when reading all those blogs, news blitzes and tech publications over the last months?

And then I started to compromise: anything exclusive to Orange, T-Mobile or 3 was out of the question (because data roaming is pretty much a killer for me), which boils it down to Blackberry and O2 or any of the others on Vodafone (which would mean that I couldn’t get what started being my favourite, the Samsung Omnia 7). Hang on: I compromise over some shoddy pounds? Is the handset then not so all important as one might have believed when reading all those blogs, news blitzes and tech publications over the last months? Anyway, back to Vodafone. They have realised (and, credit to them, admit it!) that a vertical implementation where you only get the full scope of 360 services if you have one of two phones doesn’t work. And, well, that’s somewhat obvious, isn’t it? Or is it a reasonable assumption that all my friends will all of a sudden (and at the same time) exchange their various handsets for a Samsung M1? No, I thought not either.

Anyway, back to Vodafone. They have realised (and, credit to them, admit it!) that a vertical implementation where you only get the full scope of 360 services if you have one of two phones doesn’t work. And, well, that’s somewhat obvious, isn’t it? Or is it a reasonable assumption that all my friends will all of a sudden (and at the same time) exchange their various handsets for a Samsung M1? No, I thought not either. On a sideline: I will be moderating a panel on “How to Make Money as a Developer” this week at

On a sideline: I will be moderating a panel on “How to Make Money as a Developer” this week at  Apple’s iPhone is only a marketing fad for vain urbanites. True purists go for Android. Those who see the light in volume go for Nokia or Samsung.

Apple’s iPhone is only a marketing fad for vain urbanites. True purists go for Android. Those who see the light in volume go for Nokia or Samsung. On the Nexus, you’re OK (-ish) if your life evolves around Google. With a Gmail account and associated contacts (and/or calendars), you’re sort of OK. It does all that. Now – shock, horror – I do not actually send all my mail from Gmail and my contacts are mainly dealt with in my address book (take Outlook or whatever you want if you’re a Windows user). And I use iCal and not Google Calendar. And so it starts: there is no desktop application that would help me do this. On a Mac, the phone is not even recognised when you plug it in (and that is a rare thing on a Mac; is this another piece of Apple vs. Google? I don’t know but I doubt it). So you are finding yourself setting everything up by hand! Entering the POP3 and SMTP (or IMAP) server addresses, user names, passwords, etc, etc for seven e-mail accounts is no fun. And (remember I am not a techie) invariably leads to some box checked wrongly here or a typo in a password there and, kawoom, nothing works. I can set up a Google Calendar/iCal sync BUT that will only sync the specific Google Calendar bit between the two, and not any of my other (work, home) calendars. I can sync my address book with Google, so that works. The whole procedure took me the better part of 45 minutes, including lots of corrections and swearing and led to me abandoning a half-configured beauty of an Android phone. Great result.

On the Nexus, you’re OK (-ish) if your life evolves around Google. With a Gmail account and associated contacts (and/or calendars), you’re sort of OK. It does all that. Now – shock, horror – I do not actually send all my mail from Gmail and my contacts are mainly dealt with in my address book (take Outlook or whatever you want if you’re a Windows user). And I use iCal and not Google Calendar. And so it starts: there is no desktop application that would help me do this. On a Mac, the phone is not even recognised when you plug it in (and that is a rare thing on a Mac; is this another piece of Apple vs. Google? I don’t know but I doubt it). So you are finding yourself setting everything up by hand! Entering the POP3 and SMTP (or IMAP) server addresses, user names, passwords, etc, etc for seven e-mail accounts is no fun. And (remember I am not a techie) invariably leads to some box checked wrongly here or a typo in a password there and, kawoom, nothing works. I can set up a Google Calendar/iCal sync BUT that will only sync the specific Google Calendar bit between the two, and not any of my other (work, home) calendars. I can sync my address book with Google, so that works. The whole procedure took me the better part of 45 minutes, including lots of corrections and swearing and led to me abandoning a half-configured beauty of an Android phone. Great result. My answer is: because they design it with engineer-centric design. And that is wrong! Why? Well, because most people are not engineers! An engineer thinks something along the following: I am Google and we love the cloud. Therefore, I will design everything so that it will adhere to that principle and will – in a purist kind of way – design everything in a way that you can beautifully and seamlessly set everything up – if and as long as you use all the wonderful Google services we have. And if you don’t get that, you’re not worthy.

My answer is: because they design it with engineer-centric design. And that is wrong! Why? Well, because most people are not engineers! An engineer thinks something along the following: I am Google and we love the cloud. Therefore, I will design everything so that it will adhere to that principle and will – in a purist kind of way – design everything in a way that you can beautifully and seamlessly set everything up – if and as long as you use all the wonderful Google services we have. And if you don’t get that, you’re not worthy. Apple looks at things a little differently (and it is not only for the better although, for most people, it is): they provide a tool that brings everything I need over to my phone just like that. Job done. Easy! They will look at whatever tools they need for this. And if it means extending iTunes (which, yes, I know, they had already) to accommodate syncing data other than music and video to something other than a computer, than so be it. In that, they follow their own philosophy as slavishly as the other guys do but they do design it from a people-centric rather than an engineer-centric point of view. And that is why it works so well for people that are not (also) engineers.

Apple looks at things a little differently (and it is not only for the better although, for most people, it is): they provide a tool that brings everything I need over to my phone just like that. Job done. Easy! They will look at whatever tools they need for this. And if it means extending iTunes (which, yes, I know, they had already) to accommodate syncing data other than music and video to something other than a computer, than so be it. In that, they follow their own philosophy as slavishly as the other guys do but they do design it from a people-centric rather than an engineer-centric point of view. And that is why it works so well for people that are not (also) engineers.