This is the presentation to the talk I held at the 1. Mobile e-commerce conference / Apps Summit 2010 today in Wiesbaden, Germany:

Tag: mobile Page 2 of 3

It is this time of the year where people start looking forward (and back) and come up with clever analyses of things we have always known and those that we haven’t. And because Europe has always (?) been the thoughtful and fashionably skeptic part of the world, it is that one of the leading newspapers, the Guardian, posts an article querying, gosh, Twitter. The link actually contains the words

It is this time of the year where people start looking forward (and back) and come up with clever analyses of things we have always known and those that we haven’t. And because Europe has always (?) been the thoughtful and fashionably skeptic part of the world, it is that one of the leading newspapers, the Guardian, posts an article querying, gosh, Twitter. The link actually contains the words

trouble-twitter-social-networking-banality

The proof? Iran is still not free (or so most of us Westeners think) and only 0.027% of Iranians use Twitter. There you have it. It concludes that it is all narcissistic navel-gazing. The comments, alas, are a delight to read… 🙂

Where are we then? Is this true? It is – you may have guessed that this be my stance – not. And here’s why:

![]() Social media (Twitter included) is nothing in itself, it merely defines a group of tools. Therefore, it is not the emperor’s new clothes, it is – if anything – the emperor’s new herald: if the emperor has nothing new, interesting, noteworthy to tell, it will remain as dull and meaningless as before but social tools actually allow you to filter, to focus, to spread noteworthy, sensible and truly good stuff to a group of people that is much larger than you could have reached before at a cost that is (per capita and in toto) much lower than before. And that means it is one cool tool!

Social media (Twitter included) is nothing in itself, it merely defines a group of tools. Therefore, it is not the emperor’s new clothes, it is – if anything – the emperor’s new herald: if the emperor has nothing new, interesting, noteworthy to tell, it will remain as dull and meaningless as before but social tools actually allow you to filter, to focus, to spread noteworthy, sensible and truly good stuff to a group of people that is much larger than you could have reached before at a cost that is (per capita and in toto) much lower than before. And that means it is one cool tool!

There are a gazillion reasons to dismiss Twitter (or Facebook – although fewer people seem to do just that these days) on the basis of boring info about breakfast/lunch/supper/traffic jam on way home or to hype it up on the basis of opposition in Iran/arrests in Egypt/tsunamis in Thailand or a mere plane landing on the Hudson. The argument fails both ways. It is not that. It is the fact that it is possible to communicate at nigh zero costs with people that may be interested – and it is upon the people to find you but it is also upon you to find the interesting bits!

I am already slightly tired to refer to Clay Shirky’s Here Comes Everybody who provides us with some beautiful examples of this but the point is (and here Shirky’s academic background serves him really well): it is a tool, and a tool makes only sense (or nonsense) in the hand of its user. So here’s to everyone who complains about useless and redundant info over Twitter: choose better who you follow; you would not stick around some dinner party endlessly discussing the virtues of starching napkins either, would you?

As with every tool (say, a hammer), social tools are more useful, the easier and intuitive they are to use. If it is self-explanatory on how to extract something positive (e.g. to get that bloody nail into that bloody board), the better (and if you can do it without walking away with a bloody thumb, even better). At the moment, many people walk away from Twitter because of a bloody thumb. But would you dismiss a hammer only because you hit yourself? Probably not. Unless you find a better hammer of course…

As with every tool (say, a hammer), social tools are more useful, the easier and intuitive they are to use. If it is self-explanatory on how to extract something positive (e.g. to get that bloody nail into that bloody board), the better (and if you can do it without walking away with a bloody thumb, even better). At the moment, many people walk away from Twitter because of a bloody thumb. But would you dismiss a hammer only because you hit yourself? Probably not. Unless you find a better hammer of course…

Finally (and because I called this blog “on mobile”), here’s why the combination of social tools with this other tool in everyone’s hands, namely the mobile phone, is so powerful:

- Daily circulation of newspapers worldwide: 450,000,000

- Number of TV sets in use worldwide: 1,500,000,000

- Number of Internet users worldwide: 1,600,000,000

- Number of credit cards worldwide: 1,700,000,000

- Number of toothbrushes in use worldwide: 2,250,000,000

- Number of mobile subscriptions worldwide: 4,600,000,000.

Have a great 2010!

Cartoon credit: Hugh MacLeod (http://gapingvoid.com/)

Mashable founder & CEO Peter Cashmore (who I hugely respect) declared in his recent CNN column the death of privacy and has also found the culprit, i.e he spotted

social media hold the smoking gun.

With all due respect, this could not be further from the truth (although, to be fair to him, he really only used it as an opener).

The term “social media” is self-referential and, hence, pretty meaningless.

The term “social”

refers to the interaction of organisms with other organisms and to their collective co-existence.

Media is the plural of medium, which means

something intermediate in nature or degree.

Therefore, media in the context of communication is – by definition – a tool (sic!), which connects one (human) being (also kown as the publisher) with another (also known as the user, recipient, reader, consumer, …). When “media happens”, one therefore looks at (at least) two (human) organisms interacting, which is – again by definition – social behaviour. QED.

Thou shalst not blame a tool.

To “blame” social media is akin to blaming a shotgun for dead people (and a regular reply to the latter argument would bear “interesting” implications on the former indeed, namely result in advocacy for censorship!).

When Peter Cashmore claims that social media was to blame for the loss of privacy, what he really means is that the (relatively) new tools interactive media provides users with and – maybe even more importantly – the cost of these tools (or rather the lack thereof) has led to an explosion of “publishing” activity by every man (and – PC calling – woman) and his/her dog. The published opinions of all these men and their dogs lead to the creation of something like a “meta-opinion” (which need not always be true of course: cf. the example of billions of flies eating excrements).

The core of it then is people (and lots of them) grouping their proverbial voices to create a storm. This has often been seen and some stories like the one of the Stolen Sidekick have made history. Was Sasha’s (the girl who stole the Sidekick) reputation killed by Evan’s (the guy who published the story) website? What did it then? The server? A script? Some lines of HTML code? Hardly. What it did was the overwhelming response of the public (all those men and their dogs) reacting to something Sasha (the person) had done (stole the Sidekick). And – just as a reminder – stealing something is bad!

The Tube to The Power of Mobile or: the Rise and Fall of Ian

A more recent example concerned a (now unemployed) fellow named Ian. He is a guy who appears to have a problem with anger management. Unfortunately, he worked in a customer-facing job, namely on the tube platforms in London. He lost it and had a “little” rant at a passenger (“I’ll sling you under a train”). Happens every day. BUT: it should NOT happen. Not every day, not any day!

This time, something was different, namely there was a guy standing next to him who filmed it on his mobile. He then posted this to YouTube, blogged it, twittered about it and, soon after, it was on the front pages of newspapers, online and on TV. Ian never saw it coming. Admittedly, he was particularly unfortunate that the guy filming happened to be Jonathan MacDonald, one of the more prolific and knowledgeable “social media” gurus. Suffice to say that Jonathan has a good handle on how to get word out.

Reactions to this (as well as to the Sidekick story before) were wild and (sometimes) violent, in all directions. One common outcry was the one of “trial by social media“. Hang on. What did Jonathan do? He used YouTube (which is open to everyone, including Ian), he used a blog (dito), he twittered (dito). Via Google (or any number of other tools), everyone can get the Twitter handles of newspaper editors, TV news anchors and everyone else in the “professional” media in minutes (Ian, too). A trial is one where one side (the prosecutor) prosecutes and the other side (the defendant) defends. The person that decides, however, is the judge (and/or the jury depending in which country you live).

Therefore, even if one would slap the nasty tag of “prosecutor” on Jonathan, he still was only a little piece of this. And he was NOT the judge! If there was a “trial” by any media, one could/might/wish to look at the “professional” media who picked it up although I understand that they actually have been speaking to Jonathan but also tried to get word from TfL (the tube operator) and Ian. No reply, it seems. Which is whose fault precisely?

He could have responded. TfL could actually have used this publicity to turn it around: Ian has apologised (now), TfL could have shown that they do not tolerate this AND that they are constructively tackling issues when they know of them. Jonathan even offered his collaboration in that. Alas, all London mayor Boris Johnson had to say was that he was “apalled by the video”. He did it on Twitter, mind you. How very 21st century. The tool maybe, the reaction not.

Don’t Be Evil

Google’s famous motto “Don’t Be Evil” was first smiled at as being “quaint”, then hailed as revolutionary and then queried in the face of the company “balancing” acts e.g. with a view to their self-censorship in China).

As a general motto, however, this is what is at the very heart of society. It is the motto we are all (hopefully) being brought up with. Don’t do wrong. It is, I would pose, a fairly broadly supported smallest common denominator of society.

Back in the olden days, a true gentleman would be good for his word. He would stand up in the face of evil and would defend the poor and defenceless. Honourable. And men had to be responsible for their own actions and inactions. At its core, it is all about this:

Self-responsibility is the ability to respond yourself.

Then it all went South (or so said my late grandma).

Empowered Media

Grandma would be delighted though: for we are now in a position again where the straight-forward “man and his word” (and indeed woman, too) can be re-ignited. And the driver (or, in Peter Cashmore’s words, smoking gun) is a variety of newly empowered media.

Empowered media describes the causes and effects of what we are witnessing much better than “social”: digital media become empowered by the tools (devices, software, etc.) that can be deployed to help communication – of fact and opinion – from people to people. Period.

Distinct to the ancient past of newspapers, the number of people able to “publish” has vastly increased because the costs of doing so has decreased to virtually zero. The same is true for the receiving end (which can instantly also turn into a publishing side itself). Very powerful. Also a little intimidating maybe. Well, at least if you have a problem with anger management or need otherwise a broad shoulder to hide behind.

That broad shoulder, the “excuse” by reference to some foggy higher-ups, gods in the clouds, “superiors”, etc is being removed by the ability to record and report fairly accurate accounts of actions and inactions of basically everyone. It empowers everyone (including Ian) to respond: we just re-gained the ability to respond ourselves.

Mobile is the Most Empowered

Mobile is the most powerful tool in the armoury of digital media: it is with you at all times. It is switched on at all times. It is connected at all times (well, the new generation is anyway). It can record audio and video. It can transmit audio, video and text. And it’s yours, and yours alone. And whilst it is so personal, it opens a gateway to potentially 6bn people. That’s a lot of power.

And it’s in your hand!

The good folks of Millennial Media gave me a sneak preview of their May Scorecard for Mobile Advertising Reach and Targeting (yes, they call it SMART…), which looks at the US mobile advertising market, and then my daughter broke her arm and my blogging activities (and a lot of other things) took a time-out…

Anyway, Millennial reaches 73% of all mobile Internet sites (which they claim makes them biggest), which makes it a fairly comprehensive overview. And there is a lot of interesting data buried in this brief piece of research.

So, for May 2009, the handset on which most ad impressions were recorded was not the iPhone but the Samsung “Instinct” (otherwise known as the SPH-M800). The iPhone was on #2 ahead of the Blackberry Curve. A full list of the handset breakdown looks like this:

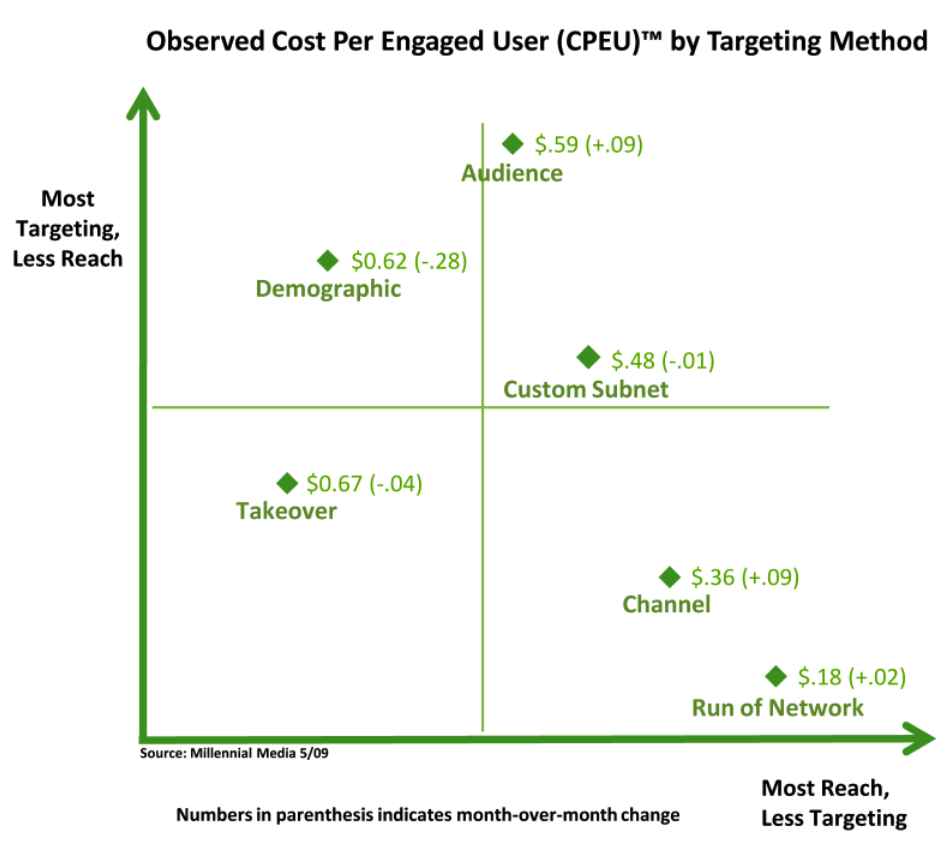

On the advertising front, we’re seeing some interesting metrics on cost per engaged user depending on the various measures included. Advertisers appear to be trying out a variety of approaches. Interestingly, the cost per engaged user for a campaign focused on a specific demographic has dropped very significantly (by ¢0.28 or c. 45%). Is this a sign of a higher take-up? Here’s a graph showing the details:

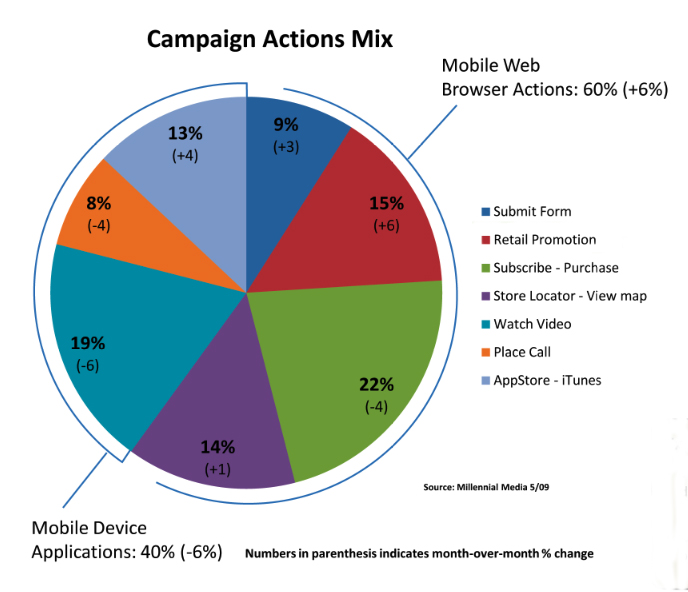

The mix of campaign activities is also interesting and shows that the sector seems to be coming of age. C. 60% of the campaigns (or committed budgets) were dedicated to the mobile web (browser) with the balance using some form of dedicated applications. The app store has its own category already and use of it (or rather iPhone apps) rose by 4 points to an overall 13% of campaigns, which is significantly higher than the iPhone’s footprint. However, I am sure more than 13% of art directors and their clients use iPhones, so maybe this is why. Or of course the iPhone could simply be a device (and the apps to go with it) that makes it easier to engage with users. Oh, what news… 😉 So here’s the final graph I’ll share with you, namely a chart showing the splits:

Mobile games blogger extraordinaire, Arjan Olsder, provided for a great guest post by Qualcomm games guru Mike Yuen, and it’s well worth a read! Mike addresses this most horrible of issues to mobile game developers that is called fragmentation or, in his words, “[t]he lack of platform and hardware standards continues to be a major inhibitor to mobile game growth in the United States [and elsewhere; ed.]. This diversity in development platforms (Android, BREW, Flash Lite, iPhone, Java, Linux, Symbian, WAP, Windows Mobile) and hardware configurations (display resolutions, RAM/heap memory size, processing and graphics power, audio formats, keypad and other input modes.”

Mobile games blogger extraordinaire, Arjan Olsder, provided for a great guest post by Qualcomm games guru Mike Yuen, and it’s well worth a read! Mike addresses this most horrible of issues to mobile game developers that is called fragmentation or, in his words, “[t]he lack of platform and hardware standards continues to be a major inhibitor to mobile game growth in the United States [and elsewhere; ed.]. This diversity in development platforms (Android, BREW, Flash Lite, iPhone, Java, Linux, Symbian, WAP, Windows Mobile) and hardware configurations (display resolutions, RAM/heap memory size, processing and graphics power, audio formats, keypad and other input modes.”

Mike rightly points out that, “[i]n many cases, the costs associated with individualizing software builds to the particularities of each handset, operator and language account for more than half of the overall development budget for new game titles. It’s a simple, but important concept. If fewer resources were diverted to porting a title from handset to handset, operator to operator, more resources could be dedicated to advancing the development of new and innovative gaming concepts.”

He goes on to draw an interesting comparison to the Korean and Japanese markets where there are not as many handsets (and platforms) around and where consumers are more than twice as likely to download mobile games. He then goes on to look at market disruptors like Apple (iPhone anyone?) and others only to conclude, sadly, that “[m]obile gaming is in a state of flux – platform and hardware fragmentation has clouded the once blue sky of gaming’s future and positive disruptive products such as Apple’s iPhone have changed industry perception and consumer expectations about the future of the mobile gaming device. I’m not expecting us to reach consensus anytime soon. Fragmentation is an inherent element of the mobile industry and perhaps always will be.”

![]() Now, is that really so? He is of course right in his analysis of the current environment. But does this really have to be like this? The mobile space suffers from too many very large companies with very large markets. And if this wasn’t enough, there’s two different groups of them, with diverging interests, namely operators (carriers) and handset manufacturers: the former want everyone to be on their network, the latter to be on their handsets. Both are more often than not big old molochs of companies with a lot of market power in their segments. However… the markets seem to gravitate (under consumer demand) towards a more open set-up: operators seem to be accepting the fact that they cannot reign their users into walled gardens forever (more and more resign to flat-rate data and open the mobile web to users) and OEMs seem to realize that they need awesome numbers of users to have a real impact and so most of them gravitate to more open platforms (or, in the case of Nokia, create them).

Now, is that really so? He is of course right in his analysis of the current environment. But does this really have to be like this? The mobile space suffers from too many very large companies with very large markets. And if this wasn’t enough, there’s two different groups of them, with diverging interests, namely operators (carriers) and handset manufacturers: the former want everyone to be on their network, the latter to be on their handsets. Both are more often than not big old molochs of companies with a lot of market power in their segments. However… the markets seem to gravitate (under consumer demand) towards a more open set-up: operators seem to be accepting the fact that they cannot reign their users into walled gardens forever (more and more resign to flat-rate data and open the mobile web to users) and OEMs seem to realize that they need awesome numbers of users to have a real impact and so most of them gravitate to more open platforms (or, in the case of Nokia, create them).

As most of the newer platforms appear to be based on C++ or siblings thereof (Symbian, UIQ, Linux, Android [yes, I know that they us a JVM], BREW, Win ME, etc), it would appear that a reduced complexity might be nigh. Not as easy as online, mind you, but light at the end of the tunnel nonetheless. And it makes sense as the current fragmentation isn’t really helping anyone: consumers grow frustrated with ever-changing platforms. They want cool content, not a proprietary operator-variant of cool content. Hope, my friends, there is hope!

As most of the newer platforms appear to be based on C++ or siblings thereof (Symbian, UIQ, Linux, Android [yes, I know that they us a JVM], BREW, Win ME, etc), it would appear that a reduced complexity might be nigh. Not as easy as online, mind you, but light at the end of the tunnel nonetheless. And it makes sense as the current fragmentation isn’t really helping anyone: consumers grow frustrated with ever-changing platforms. They want cool content, not a proprietary operator-variant of cool content. Hope, my friends, there is hope!

![]() Here‘s a really good piece of analysis of the landscape of mobile social networks. I will not recount the findings in detail here but they reckon that the Internet biggies Facebook and MySpace rule the mobile social networking world already. MySpace is said to have had 1.4bn visits last month alone. Facebook also is beyond the 1bn mark. Impressive numbers! The largest pure mobile-play, Mocospace, a predominantly US-focussed company, recorded 1bn visits.

Here‘s a really good piece of analysis of the landscape of mobile social networks. I will not recount the findings in detail here but they reckon that the Internet biggies Facebook and MySpace rule the mobile social networking world already. MySpace is said to have had 1.4bn visits last month alone. Facebook also is beyond the 1bn mark. Impressive numbers! The largest pure mobile-play, Mocospace, a predominantly US-focussed company, recorded 1bn visits.

The article does mention GoFresh (with their ItsMy service) and Peperonity but fails to point out UK company Yospace who power the combined O2/3UK community.

Whilst the mobile-only players all point out that they’re not worried because their offering was better (“he would say that, wouldn’t he, your Honour?”), but advertising muscle may well be an issue: MySpace recently said that they would expect about half of their total traffic coming from mobile within 5 years, and reaffirmed that mobile is one of the most important strategic initiatives for MySpace. I am sure there will be loads of niches in the sector but the bulk of 1.5bn visits (probably steeply rising) is a tough proposition to beat when it comes to ad revenues!

Whilst the mobile-only players all point out that they’re not worried because their offering was better (“he would say that, wouldn’t he, your Honour?”), but advertising muscle may well be an issue: MySpace recently said that they would expect about half of their total traffic coming from mobile within 5 years, and reaffirmed that mobile is one of the most important strategic initiatives for MySpace. I am sure there will be loads of niches in the sector but the bulk of 1.5bn visits (probably steeply rising) is a tough proposition to beat when it comes to ad revenues!